Upgrading to Workspace

We will be discontinuing the Eikon Desktop soon in favour of our next generation data and analytics workflow solution, LSEG Workspace. This page is designed to help you assess any changes you may need to make to programmatic (API) workflows. We also provide resources here to help you make those changes as well.

Upgrading to Workspace

Other related resources

Custom Application COM API Upgrade:

DEX2.dll

Prerequisites

COM Prerequisites

Documentation on using the COM API in the Microsoft Office suite is available here: COM APIs for Microsoft Office. Users were also able to use the COM APIs outside of Microsoft Office suite for example in a standalone app: COM APIs for use in custom applications. A list of the prerequisites in question can be found in the index of this article.

If you are new to Python, don't hesitate to install it on your machine and try it out yourself as outlined in this 3rd party tutorial. Otherwise, you can simply use Codebook as outlined in this Tutorial Video.

Python works with libraries that one can import to use functionalities that are not natively supported by the base coding package. Some popular distributuions of python include many of the popular packages that one could use for various tasks - Anaconda is the most popular such distribution.

The RD Library allows for code portability across the desktop and enterprise platforms - with only small changes in authentication credentials. These credentials are stored in a config file - but if you are just using the desktop you need not concern yourself with this as a desktop session is the default credential setup.

Open a new single sheet Excel workbook.

Save As with an appropriate name (e.g. AdxRtSourceList.xls or AdxRtSourceList.xlsm in Office 2007 or higher).

Go to the VBE (Visual Basic Editor), ensure the Project Explorer is visible and select the project for the workbook.

<ALT><F11> or Tools, Macro, Visual Basic Editor in Excel 2003 or Developer, Visual Basic in Excel 2007 and above, View, Project Explorer If the Developer header is not visible in Excel 2007 and above, go to the Excel Office Button, select Excel Options (lower right), Popular, and check the 'Show Developer tab in the Ribbon' box.

In the VBE, click on File, Import File and import PLVbaApis.bas.

The .bas location is C:\Program Files (x86)\Thomson Reuters\Eikon\Z\Bin (Z may be X or Y, depending on the last Eikon update). The .bas is loaded as a new VB project module, PLVbaApis.

In the PLVbaAPis module, comment out the sections which aren't required.

E.G.: when dealing with AdxRtSourceList, part of the real time library AdfinXRtLib, the AdfinX Real Time section can remain uncommented.

In the VBE, go Tools, References and ensure that AdfinX Real Time Library is checked.

If it is not in the list the library is called rtx.dll and its location for Eikon 4 is ">C:\Program Files (x86)\Thomson Reuters\Eikon\Z\Bin (Z may be X or Y, depending on the last Eikon update).

import refinitiv.data as rd # pip install httpx==0.21.3 # !pip install refinitiv.data --upgrade

from refinitiv.data.discovery import Chain

from refinitiv.data.content import search

import pandas as pd

pd.set_option('display.max_columns', None)

import numpy as np

import os

import time

import datetime # `datetime` allows us to manipulate time as we would data-points.

from IPython.display import display, clear_output # `IPython` here will allow us to plot grahs and the likes.

rd.open_session("desktop.workspace")

<refinitiv.data.session.Definition object at 0x7fa34230ac18 {name='workspace'}>

DEX2.dll

The DEX2.dll COM API component provides access to a broad range of fundamental and reference data (including all the TR.xxx fields). The RData Excel function provided both Fundamental and Reference as well as streaming realtime prices and news using this component under the hood along with RTX.dll.

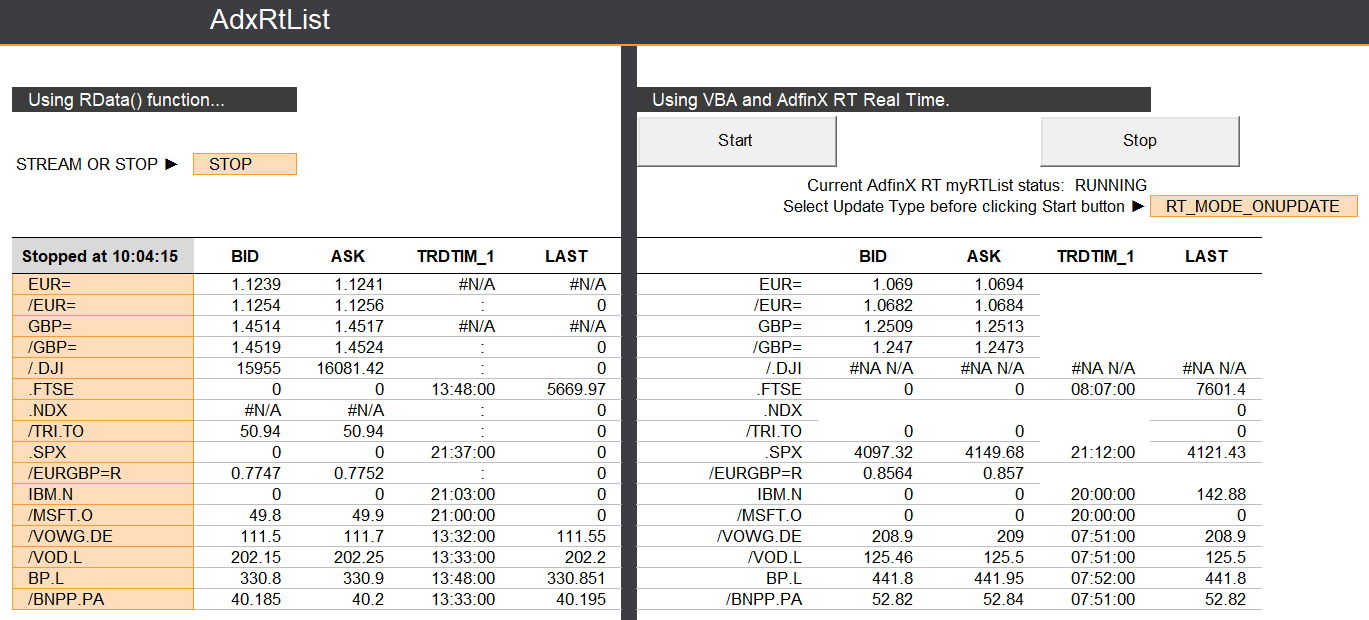

Rdata List Realtime

When using the old COM API to get Rdata List data, one may be greeted with an Excel sheet that looks like this:

VBA

In VBA, this was done with a function akin to .StartUpdates RT_MODE_ONUPDATE & myRTList = CreateAdxRtList(), e.g.:

With myRTList

.ErrorMode = EXCEPTION

' N.B.! Source name may need to be changed if not named as below!

.Source = "IDN" '_SELECTFEED"

' Register the items and fields

.RegisterItems ItemArray, FieldArray

' Set the user tag on each item. This helps indexing the results

' table for displaying the data in the callback

For m = LBound(ItemArray) To UBound(ItemArray)

.UserTag(ItemArray(m), "*") = m

For n = LBound(FieldArray) To UBound(FieldArray)

.UserTag(ItemArray(m), FieldArray(n)) = n

Next n

Next m

.Mode = "TIMEOUT:5"

' If timed basis desired, then FRQ setting and RT_MODE_ONTIME or RT_MODE_ONTIME_IF_UPDATED required,

' which will trigger the OnUpdate event, shown below.

'.Mode = "FRQ:2S"

' And, finally, request the data!

Select Case Range("dcUpdateType").Value

Case "RT_MODE_IMAGE"

.StartUpdates RT_MODE_IMAGE

Case "RT_MODE_ONUPDATE"

.StartUpdates RT_MODE_ONUPDATE

End Select

'.StartUpdates RT_MODE_ONUPDATE

'.StartUpdates RT_MODE_IMAGE

'Other modes shown below; different events will be fired.

'.StartUpdates RT_MODE_ONTIME, RT_MODE_ONTIME_IF_UPDATED, RT_MODE_ONTIME,

' RT_MODE_ONUPDATE, RT_MODE_IMAGE , RT_MODE_NOT_SET

End With

To stop this update, you would have to create some VBA code to (e.g.: Sub cmdStop_Click()), but that is simpler in Python with stream.close():

However - many developers also used the RData worksheet function object directly in VBA.

Python

Here we have a data-frame of instruments and fields updating live every x seconds, let's say (for the sake of the use-case example) every 3 seconds. This is simple to recreate in Python:

#define stream

stream = rd.open_pricing_stream(

universe=['GBP=', 'EUR=', 'JPY=', '.GDAXI', '.FTSE', '.NDX', 'TRI.TO', 'EURGBP=R'],

fields=['CF_TIME', 'CF_LAST', 'BID', 'ASK', 'TRDTIM_1'])

#open stream

stream.open()

<OpenState.Opened: 'Opened'>

#add temporal update functionality using stream.get_snapshot

now = time.perf_counter()

while time.perf_counter() < now + 30:

time.sleep(3)

clear_output(wait=True)

df = stream.get_snapshot(

universe=['GBP=', 'EUR=', 'JPY=', '.GDAXI', '.FTSE', '.NDX', 'TRI.TO', 'EURGBP=R'],

fields=['CF_TIME', 'CF_LAST', 'BID', 'ASK', 'TRDTIM_1'])

display(df)

| Instrument | CF_TIME | CF_LAST | BID | ASK | TRDTIM_1 | |

| 0 | GBP= | 11:44:36 | 1.1983 | 1.1983 | 1.1987 | <NA> |

| 1 | EUR= | 11:44:36 | 1.0657 | 1.0657 | 1.0661 | <NA> |

| 2 | JPY= | 11:44:37 | 136.02 | 136.02 | 136.03 | <NA> |

| 3 | .GDAXI | 11:44:00 | 15677.13 | <NA> | <NA> | 11:44:00 |

| 4 | .FTSE | 11:44:00 | 7948.93 | <NA> | <NA> | 11:44:00 |

| 5 | .NDX | 22:15:59 | 12302.48 | <NA> | <NA> | <NA> |

| 6 | TRI.TO | 21:00:00 | 165.81 | 162.61 | 167 | <NA> |

| 7 | EURGBP=R | 11:44:37 | 0.889 | 0.889 | 0.8897 | <NA> |

Close the stream

stream.close()

<OpenState.Closed: 'Closed'>

Create a Streaming Price and register event callbacks using RDP

You can build upon the example above, using the RD Library Example notebook present in Codebook that demonstrates how to use a StreamingPrice with events to update a Pandas DataFrame with real-time streaming data. Using a StreamingPrices object that way allows your application to have at its own in memory representation (a Pandas DataFrame in this example) that is kept updated with the latest streaming values received from Eikon or Refinitiv Workspace. Here we're putting ourselves in the shoes of a Foreign eXchange (FX) trader looking at Emerging Market (EM) currency exchange rates; e.g: the Nigerian Nairas (NGN) and Indonesian Rupiah (IDR).

You can find the code for this on GitHub here.

RData Function

What does RData do?

RData is a flexible excel worksheet function allowing access to realtime and fundamental & reference data content. It can also be used programatcally in VBA and the results then dumped to an excel range for example.

VBA

For VBA related to Fundamental data, please see the 'DEX2 Fundamental and Reference' section below.

Python

We have separated getting current fundamental snapshots - using a rd.get_data function and getting historical fundamental timeseries using either the rd.get_data function or the rd.get_history() function.

Snapshot requests

For snapshot current fundamental requests - things are pretty straight forward - select your universe of instruments and then the list of fields you want. A full list of fields is available using the Data Item Browser App (type DIB into Eikon or Workspace search bar).

df1 = rd.get_data(

universe=['BARC.L', 'TRI.N', 'TSLA.O'],

fields=['TR.RevenueMean.date', 'TR.RevenueMean', 'TR.TRBCEconomicSector',

'TR.TRBCEconSectorCode', 'TR.TRBCBusinessSector',

'TR.TRBCBusinessSectorCode', 'TR.TRBCIndustryGroup',

'TR.TRBCIndustryGroupCode', 'TR.TRBCIndustry', 'TR.TRBCIndustryCode'])

df1

| Instrument | Date | Revenue - Mean | TRBC Economic Sector Name | TRBC Economic Sector Code | TRBC Business Sector Name | TRBC Business Sector Code | TRBC Industry Group Name | TRBC Industry Group Code | TRBC Industry Name | TRBC Industry Code | |

| 0 | BARC.L | 06/03/2023 | 26185926370 | Financials | 55 | Banking & Investment Services | 5510 | Banking Services | 551010 | Banks | 55101010 |

| 1 | TRI.N | 22/02/2023 | 6937020650 | Industrials | 52 | Industrial & Commercial Services | 5220 | Professional & Commercial Services | 522030 | Professional Information Services | 52203070 |

| 2 | TSLA.O | 05/03/2023 | 1.03134E+11 | Consumer Cyclicals | 53 | Automobiles & Auto Parts | 5310 | Automobiles & Auto Parts | 531010 | Auto & Truck Manufacturers | 53101010 |

If we want to add some fundamental history to this request - we can add a parameters section to the get_data request - as below which will give us the last 4 fiscal years ('FRQ': 'FY') of history for each RIC. Note for static reference fields such sector codes - these will not be published as a timeseries history - however, we can forward fill as shown below.

df1 = rd.get_data(

universe=['BARC.L', 'TRI.N', 'TSLA.O', Peers('HD'), Customers],

fields=[

'TR.RevenueMean.date', 'TR.RevenueMean',

'TR.TRBCEconomicSector', 'TR.TRBCEconSectorCode', 'TR.TRBCBusinessSector',

'TR.TRBCBusinessSectorCode', 'TR.TRBCIndustryGroup', 'TR.TRBCIndustryGroupCode',

'TR.TRBCIndustry', 'TR.TRBCIndustryCode'],

parameters={'SDate': 0, 'EDate': -3, 'FRQ': 'FY'}

)

df1

|

Instrument | Date | Revenue - Mean | TRBC Economic Sector Name | TRBC Economic Sector Code | TRBC Business Sector Name | TRBC Business Sector Code | TRBC Industry Group Name | TRBC Industry Group Code | TRBC Industry Name | TRBC Industry Code |

| 0 | BARC.L | 06/03/2023 | 26185926370 | Financials | 55 | Banking & Investment Services | 5510 | Banking Services | 551010 | Banks | 55101010 |

| 1 | BARC.L | 13/02/2023 | 25107439220 | ||||||||

| 2 | BARC.L | 11/02/2022 | 21896182240 | ||||||||

| 3 | BARC.L | 28/01/2021 | 21603248110 | ||||||||

| 4 | TRI.N | 22/02/2023 | 6937020650 | Industrials | 52 | Industrial & Commercial Services | 5220 | Professional & Commercial Services | 522030 | Professional Information Services | 52203070 |

| 5 | TRI.N | 01/02/2023 | 6626869820 | ||||||||

| 6 | TRI.N | 07/02/2022 | 6311529500 | ||||||||

| 7 | TRI.N | 22/02/2021 | 5980789530 | ||||||||

| 8 | TSLA.O | 05/03/2023 | 1.03134E+11 | Consumer Cyclicals | 53 | Automobiles & Auto Parts | 5310 | Automobiles & Auto Parts | 531010 | Auto & Truck Manufacturers | 53101010 |

| 9 | TSLA.O | 25/01/2023 | 81715341140 | ||||||||

| 10 | TSLA.O | 25/01/2022 | 52595085190 | ||||||||

| 11 | TSLA.O | 27/01/2021 | 31012329500 |

# The below in this cell is needed to forward fill our dataframe correctly:

df1.replace({'': np.nan}, inplace=True)

df1.where(pd.notnull(df1), np.nan, inplace=True)

for i in df1.groupby(by=["Instrument"]):

if i[0] == df1["Instrument"][0]: _df1 = i[1].ffill()

else: _df1 = _df1.append(i[1].ffill())

_df1

| Instrument | Date | Revenue - Mean | TRBC Economic Sector Name | TRBC Economic Sector Code | TRBC Business Sector Name | TRBC Business Sector Code | TRBC Industry Group Name | TRBC Industry Group Code | TRBC Industry Name | TRBC Industry Code | |

| 0 | BARC.L | 06/03/2023 | 26185926370 | Financials | 55 | Banking & Investment Services | 5510 | Banking Services | 551010 | Banks | 55101010 |

| 1 | BARC.L | 13/02/2023 | 25107439220 | Financials | 55 | Banking & Investment Services | 5510 | Banking Services | 551010 | Banks | 55101010 |

| 2 | BARC.L | 11/02/2022 | 21896182240 | Financials | 55 | Banking & Investment Services | 5510 | Banking Services | 551010 | Banks | 55101010 |

| 3 | BARC.L | 28/01/2021 | 21603248110 | Financials | 55 | Banking & Investment Services | 5510 | Banking Services | 551010 | Banks | 55101010 |

| 4 | TRI.N | 22/02/2023 | 6937020650 | Industrials | 52 | Industrial & Commercial Services | 5220 | Professional & Commercial Services | 522030 | Professional Information Services | 52203070 |

| 5 | TRI.N | 01/02/2023 | 6626869820 | Industrials | 52 | Industrial & Commercial Services | 5220 | Professional & Commercial Services | 522030 | Professional Information Services | 52203070 |

| 6 | TRI.N | 07/02/2022 | 6311529500 | Industrials | 52 | Industrial & Commercial Services | 5220 | Professional & Commercial Services | 522030 | Professional Information Services | 52203070 |

| 7 | TRI.N | 22/02/2021 | 5980789530 | Industrials | 52 | Industrial & Commercial Services | 5220 | Professional & Commercial Services | 522030 | Professional Information Services | 52203070 |

| 8 | TSLA.O | 05/03/2023 | 1.03134E+11 | Consumer Cyclicals | 53 | Automobiles & Auto Parts | 5310 | Automobiles & Auto Parts | 531010 | Auto & Truck Manufacturers | 53101010 |

| 9 | TSLA.O | 25/01/2023 | 81715341140 | Consumer Cyclicals | 53 | Automobiles & Auto Parts | 5310 | Automobiles & Auto Parts | 531010 | Auto & Truck Manufacturers | 53101010 |

| 10 | TSLA.O | 25/01/2022 | 52595085190 | Consumer Cyclicals | 53 | Automobiles & Auto Parts | 5310 | Automobiles & Auto Parts | 531010 | Auto & Truck Manufacturers | 53101010 |

| 11 | TSLA.O | 27/01/2021 | 31012329500 | Consumer Cyclicals | 53 | Automobiles & Auto Parts | 5310 | Automobiles & Auto Parts | 531010 | Auto & Truck Manufacturers | 53101010 |

Snapshot Requests Tip 1

Some fundamental fields will give multiple rows for a given day - for example if we request ratings sources - there could be more than one per date eg if there are 5 ratings agencies providing a rating - this is not usual for a time series history - or perhaps it is very different say than non-expandable single point timeseries. In this example as we have multiple RICS whose ratings dates may not overlap ie be on the same row <NA> artifacts are added to deliver the dataframe

df2 = rd.get_history(

universe=['BARC.L', 'TRI.N','TSLA.O'],

fields=['TR.IR.RatingSourceDescription', 'TR.IR.RatingSourceType',

'TR.IR.Rating','TR.IR.Rating.date'],

interval="1Y",

start="2015-01-25",

end="2022-02-01")

df2

| BARC.L | … | TSLA.O | |||||||

| Rating Source Description | Rating Source Type | Issuer Rating | Date | … | Rating Source Description | Rating Source Type | Issuer Rating | Date | |

| Date | … | ||||||||

| 16/07/2015 | <NA> | <NA> | <NA> | NaT | … | <NA> | <NA> | <NA> | NaT |

| 19/11/2015 | Fitch Senior Unsecured | FSU | A | 19/11/2015 | … | <NA> | <NA> | <NA> | NaT |

| 19/11/2015 | Fitch Short-term Debt Rating | FDT | F1 | 19/11/2015 | … | <NA> | <NA> | <NA> | NaT |

| 16/08/2016 | <NA> | <NA> | <NA> | NaT | … | <NA> | <NA> | <NA> | NaT |

| 12/12/2016 | Moody's Long-term Issuer Rating | MIS | Baa2 | 12/12/2016 | … | <NA> | <NA> | <NA> | NaT |

| 12/12/2016 | Moody's Long-term Senior Unsecured MTN Rating | MMU | (P)Baa2 | 12/12/2016 | … | <NA> | <NA> | <NA> | NaT |

| … | … | … | … | … | … | … | … | … | … |

| 22/10/2021 | <NA> | <NA> | <NA> | NaT | … | S&P Senior Unsecured | SSU | BB+ | 22/10/2021 |

| 26/11/2021 | R&I Long-term Issuer Rating | RII | A | 26/11/2021 | … | <NA> | <NA> | <NA> | NaT |

df2 = rd.get_history(

universe=['BARC.L', 'TRI.N', 'TSLA.O'],

fields=['TR.RecEstValue', 'TR.TPEstValue', 'TR.EPSEstValue'],

interval="1M",

start="2020-01-25",

end="2022-02-01")

df2

| BARC.L | TRI.N | TSLA.O | |||||||

| Standard Rec (1-5) - Broker Estimate | Target Price - Broker Estimate | Earnings Per Share - Broker Estimate | Standard Rec (1-5) - Broker Estimate | Target Price - Broker Estimate | Earnings Per Share - Broker Estimate | Standard Rec (1-5) - Broker Estimate | Target Price - Broker Estimate | Earnings Per Share - Broker Estimate | |

| Date | |||||||||

| 02/10/2013 00:00 | 2 | <NA> | <NA> | <NA> | <NA> | <NA> | <NA> | <NA> | <NA> |

| 02/10/2013 00:00 | 2 | <NA> | <NA> | <NA> | <NA> | <NA> | <NA> | <NA> | <NA> |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 31/01/2022 21:05 | <NA> | <NA> | <NA> | <NA> | <NA> | <NA> | <NA> | 326.66633 | 4.28333 |

| 31/01/2022 23:00 | <NA> | <NA> | <NA> | <NA> | <NA> | <NA> | <NA> | <NA> | 4.84999 |

DEX2

What does this do?

The DEX2 interface provided a broad range of content and functionality such Fundamental and Reference as well as timeseries histories of such fields. The DEX2 interface also provided interday timeseries histories for both realtime and non-realtime data. In addition you could use it for symbology conversion.

DEX2 ID to RIC (Symbology Conversion)

As shown in Tutorial 6 - Data Engine - Dex2's Excel Workbook, we can convert symbols using the COM API.

VBA

After setting MyDex2Mgr = CreateReutersObject("Dex2.Dex2Mgr"), for ISINs, we can then go ahead with

' Must call Initialise() at once

m_cookie = MyDex2Mgr.Initialize()

' We can then create an RData object

Set myRData1 = MyDex2Mgr.CreateRData(m_cookie)

With MyDex2Mgr .SetErrorHandling m_cookie, DE_EH_STRING ' Could also use DE_EH_ERRORCODES End With

' Set the properties & methods for the DEX2Lib.RData object With myRData1 .InstrumentIDList = Range("B7").Value ' Could use "TRI.N", "TRI.N; GOOG.O; MSFT.O" or array, e.g. arrInstrList. .FieldList = Range("D7").Value & "; " & Range("D8").Value '"RI.ID.RIC; RI.ID.ISIN" ' Could use "RI.ID.RIC", "RI.ID.RIC; RI.ID.WERT" or array, e.g. arrFldList. .DisplayParam = "Transpose:Y" 'N.B. Could use .SetParameter "TRI.N; MSFT.O","RF.G.COMPNAME; RF.G.NUMEMPLOY; RF.G.CNTEMAIL", "", "RH:In CH:Fd Transpose:Y" 'Hence .SetParameter [InstrumentIDList].Value, [FieldList].Value, [RequestParam].Value, [DisplayParam].Value

'Ignore cache; get data directly from the Snapshot Server '.Subscribe False 'Or use cache by default .Subscribe End With Exit Sub

For SEDOL, we can use:

' Must call Initialise() at once

m_cookie = MyDex2Mgr.Initialize()

' We can then create an RData object

Set myRData2 = MyDex2Mgr.CreateRData(m_cookie)

With MyDex2Mgr .SetErrorHandling m_cookie, DE_EH_STRING ' Could also use DE_EH_ERRORCODES End With

' Set the properties & methods for the DEX2Lib.RData object With myRData2 .InstrumentIDList = [B10].Value ' Could use "TRI.N", "TRI.N; GOOG.O; MSFT.O" or array, e.g. arrInstrList. .FieldList = Range("D10").Value & "; " & Range("D11").Value '"RI.ID.RIC; RI.ID.SEDOL" ' Could use "RI.ID.RIC", "RI.ID.RIC; RI.ID.WERT" or array, e.g. arrFldList. .DisplayParam = "Transpose:Y" 'N.B. Could use .SetParameter "TRI.N; MSFT.O","RF.G.COMPNAME; RF.G.NUMEMPLOY; RF.G.CNTEMAIL", "", "RH:In CH:Fd Transpose:Y" 'Hence .SetParameter [InstrumentIDList].Value, [FieldList].Value, [RequestParam].Value, [DisplayParam].Value

'Ignore cache; get data directly from the Snapshot Server '.Subscribe False 'Or use cache by default .Subscribe End With Exit Sub

Python

Symbology conversions in python are a lot more powerful than in Excel using the COM API. The extent of the use-cases for symbology conversions are best explained in our GitHub Repository, but for the sake of completeness, you can see an example use in the 2 cells directly below:

# # Get generic table of many symbols for 4 companies of choice:

from refinitiv.data.content import symbol_conversion

response = symbol_conversion.Definition(symbols=["MSFT.O", "AAPL.O", "GOOG.O", "IBM.N"]).get_data()

response.data.df

| DocumentTitle | RIC | IssueISIN | CUSIP | SEDOL | TickerSymbol | IssuerOAPermID | |

| MSFT.O | Microsoft Corp, Ordinary Share, NASDAQ Global ... | MSFT.O | US5949181045 | 594918104 | <NA> | MSFT | 4295907168 |

| AAPL.O | Apple Inc, Ordinary Share, NASDAQ Global Selec... | AAPL.O | US0378331005 | 37833100 | <NA> | AAPL | 4295905573 |

| GOOG.O | Alphabet Inc, Ordinary Share, Class C, NASDAQ ... | GOOG.O | US02079K1079 | 02079K107 | <NA> | GOOG | 5030853586 |

| IBM.N | International Business Machines Corp, Ordinary... | IBM.N | US4592001014 | 459200101 | 2005973 | IBM | 4295904307 |

# # Convert specific symbols:

response = symbol_conversion.Definition(

symbols=["US5949181045", "US02079K1079"],

from_symbol_type= symbol_conversion.SymbolTypes.ISIN, # Symbol types: RIC => RIC; ISIN => IssueISIN; CUSIP => CUSIP; SEDOL => SEDOL; TICKER_SYMBOL => TickerSymbol; OA_PERM_ID => IssuerOAPermID; LIPPER_ID => FundClassLipperID

to_symbol_types=[symbol_conversion.SymbolTypes.RIC,

symbol_conversion.SymbolTypes.OA_PERM_ID],

).get_data()

response.data.df

| DocumentTitle | RIC | IssuerOAPermID | |

| US5949181045 | Microsoft Corp, Ordinary Share, NASDAQ Global ... | MSFT.O | 4295907168 |

| US02079K1079 | Alphabet Inc, Ordinary Share, Class C, NASDAQ ... | GOOG.O | 5030853586 |

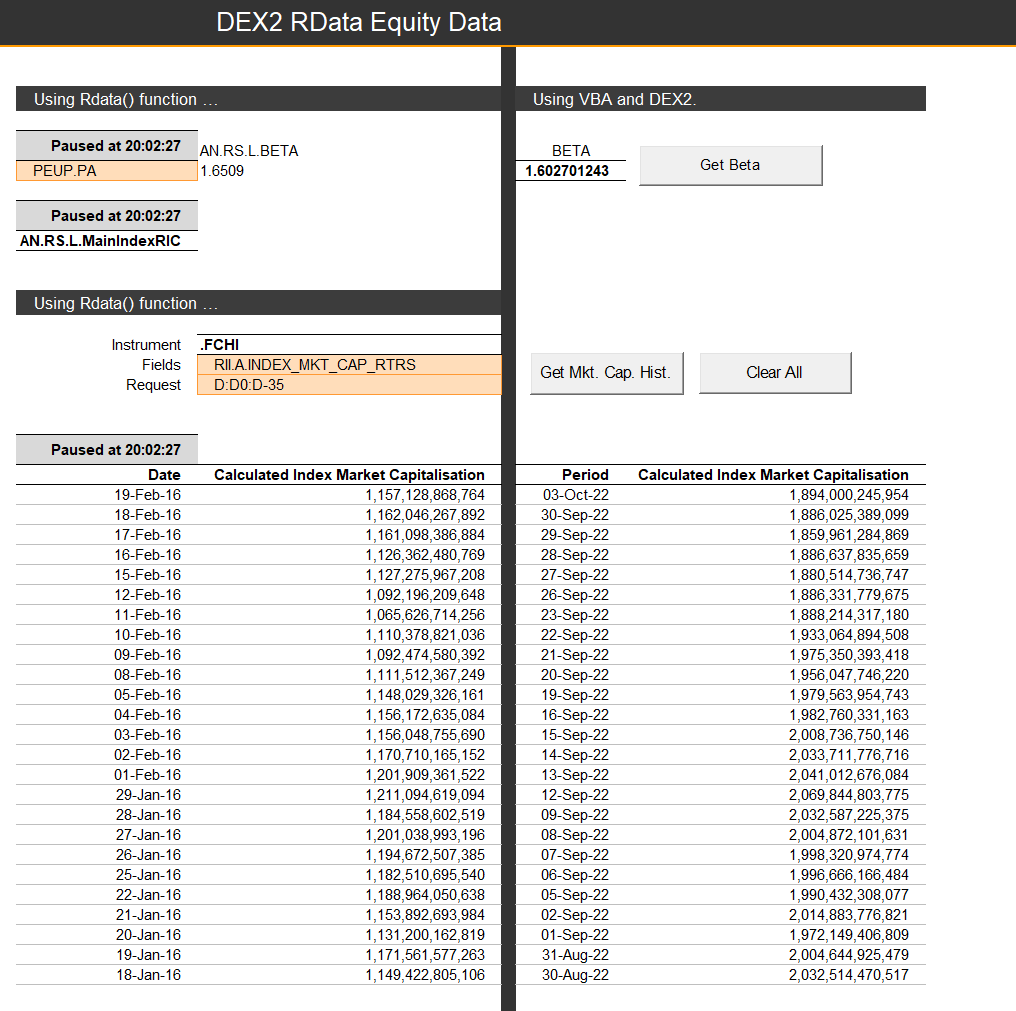

DEX2 RData Equity Data

As best exemplified in Tutorial 6 - Data Engine - Dex2's Excel Workbook, the DEX2 RData Equity Data allows us to access historical Market Capital:

VBA

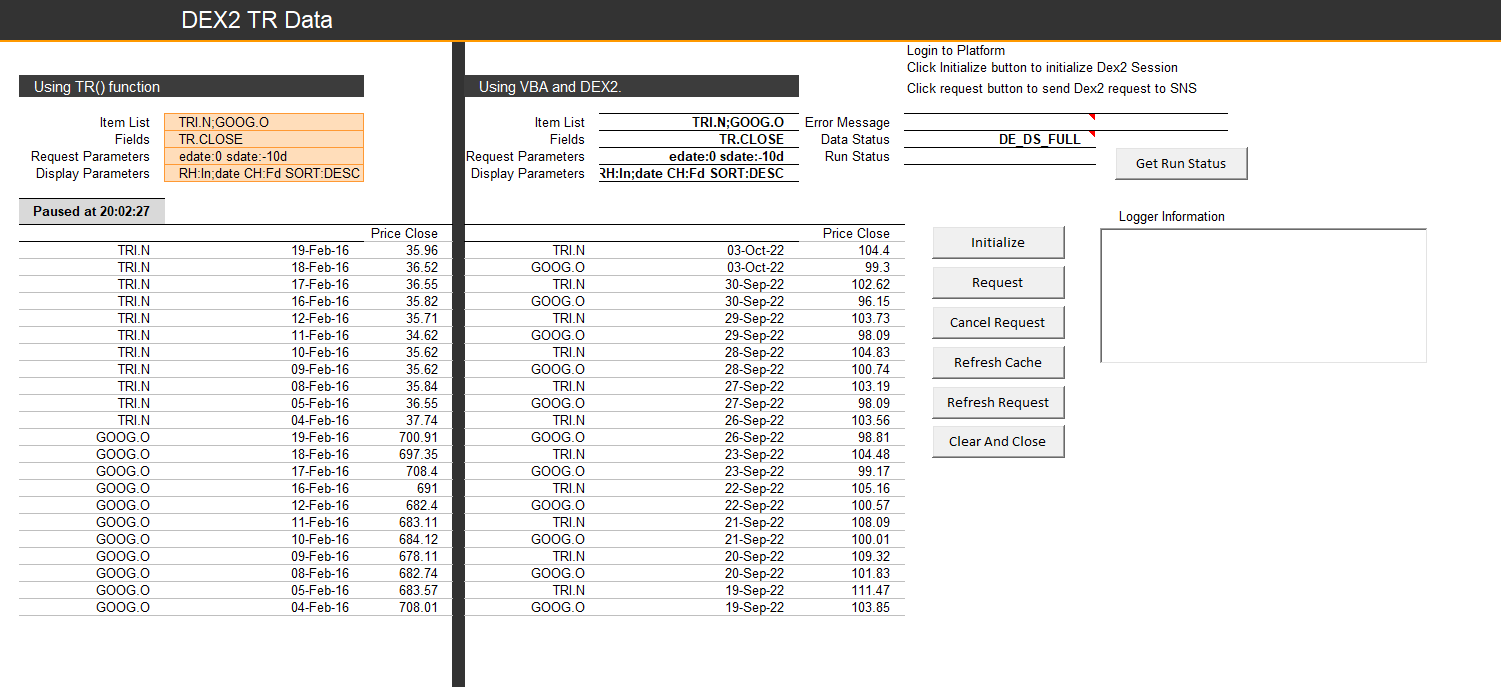

DEX2 replicates RData() and TR() functions for real time data retrieval in Eikon for Excel / Eikon - Microsoft Office. The DEX2 methods differ slightly in the initialisation and use of the Dex2Mgr object depending upon whether RData() or the TR() function is being replicated. The examples below explain this. The TR() function can be used to retrieve data from ADC (the Analytics Data Cloud) and this is contained in Tutorial 11 - Dex2 TR function Analytics Data Cloud ADC data here.

NOTE - Eikon for Excel or Eikon - Microsoft Office should be logged in otherwise the sample VBA code will generate an error "ERROR #360c - AdxRtx : No connection to the platform".

Create an instance of an DEX2Mgr object using the PLVbaApis function CreateDex2Mgr().

Set myDEX2Mgr = CreateDex2Mgr()

To replicate RData(), create the Dex2Mgr object (myDex2Mgr) and initialise it. Use the return value from the initialisation to create an instance of the Dex2Lib.RData Class (myDex2RData) using the CreateRData method.

Now go ahead with cmdMktCapHist_Click creation:

Private Sub cmdMktCapHist_Click() On Error GoTo errHandler

ActiveCell.Select

Range("F20:G100").ClearContents If MyDex2Mgr Is Nothing Then Set MyDex2Mgr = CreateReutersObject("Dex2.Dex2Mgr")

' Must call Initialise() at once m_cookie = MyDex2Mgr.Initialize() ' We can then create an RData object Set myRData2 = MyDex2Mgr.CreateRData(m_cookie)

With MyDex2Mgr .SetErrorHandling m_cookie, DE_EH_STRING ' Could also use DE_EH_ERROR_CODES End With

' Set the properties & methods for the DEX2Lib.RData object. With myRData2 .InstrumentIDList = [C15].Value .FieldList = [C16].Value '"RII.A.INDEX_MKT_CAP_RTRS" '"RII.A.INDEX_MKT_CAP_RTRS; RII.A.INDEX_MKT_CAP_USDRTRS" ' Could use single "RI.ID.RIC", multiple "RI.ID.RIC; RI.ID.WERT" or array, e.g. arrFldList. .RequestParam = [C17].Value .DisplayParam = "RH:D CH:Fd SORT:DESC" 'N.B. Could use .SetParameter "TRI.N; MSFT.O","RF.G.COMPNAME; RF.G.NUMEMPLOY; RF.G.CNTEMAIL", "", "RH:In CH:Fd Transpose:Y" 'Hence .SetParameter [InstrumentIDList].Value, [FieldList].Value, [RequestParam].Value, [DisplayParam].Value

'Ignore cache; get data directly from the Snapshot Server '.Subscribe False 'Or use cache by default .Subscribe End With Exit Sub

errHandler: MsgBox MyDex2Mgr.GetErrorString(Err.Number) End Sub

' OnUpdate event callback for myRData1 Private Sub myRData2_OnUpdate(ByVal DataStatus As Dex2Lib.DEX2_DataStatus, ByVal Error As Variant) Dim C As Integer, r As Integer Dim res2 As Variant

If Error <> 0 Then [F21].Value = Error: Exit Sub

res2 = myRData2.Data

If IsEmpty(res2) Then [F21].Value = "No data": Exit Sub

' r for the rows For r = LBound(res2, 1) To UBound(res2, 1) ' c for the columns For C = LBound(res2, 2) To UBound(res2, 2) [F21].Offset(r, C).Value = res2(r, C) Next C Next r End Sub

Python

Couldn't be easier in Python:

MarketCapDf = rd.get_history(

universe=['VOD.L','BARC.L'],

fields=['TR.CompanyMarketCapitalization'],

interval="1D", # The consolidation interval. Supported intervals are: tick, tas, taq, minute, 1min, 5min, 10min, 30min, 60min, hourly, 1h, daily, 1d, 1D, 7D, 7d, weekly, 1W, monthly, 1M, quarterly, 3M, 6M, yearly, 1Y.

start="2022-08-10",

end="2022-09-13")

MarketCapDf

| Company Market Capitalization |

VOD.L | BARC.L |

| Date | ||

| 10/08/2022 | 33802223010 | 27530345491 |

| 11/08/2022 | 33794859479 | 27383302388 |

| … | … | … |

| 12/09/2022 | 30687668213 | 27864039079 |

| 13/09/2022 | 30275827985 | 27526300175 |

VBA

You'd have to Initialize Dex2 session under the sub cmdInitialize_Click():

' Initialize Dex2 session when the data request is first started. Private Sub cmdInitialize_Click() On Error GoTo ErrorHandle

ActiveCell.Select

' Clear the output of logger lbLog.Clear

ClearAllOutput

' Clear the Cookie and old query If Not MyDex2Cookie = 0 Then MyDex2Mgr.Finalize (MyDex2Cookie) MyDex2Cookie = 0 Set MyDex2Mgr = Nothing Set MyDex2RData = Nothing End If

' Instantiate the Dex2 manager Set MyDex2Mgr = CreateDex2Mgr() Set MyDex2MgrADC = MyDex2Mgr ' Instantiate the RSearch logger Set MyDex2Logger = New CLogger

' Initialize Dex2 session MyDex2Cookie = MyDex2MgrADC.Initialize(DE_MC_ADC_POWERLINK, MyDex2Logger)

' We can choose to display error code MyDex2Mgr.SetErrorHandling MyDex2Cookie, DE_EH_ERROR_CODES ' Or display error description ' MyDex2Mgr.SetErrorHandling MyDex2Cookie, DE_EH_STRING

' Create a Dex2 query using the session cookie Set MyDex2RData = MyDex2Mgr.CreateRData(MyDex2Cookie)

' Create a Dex2 query manager using the session cookie Set MyDex2RDataMgr = MyDex2Mgr.CreateRDataMgr(MyDex2Cookie)

Exit Sub

Python

In Python, things are a little simpler:

DEX2Df = rd.get_history(

universe=['VOD.L', 'BARC.L', 'TRI.N'],

fields=['TR.TotalReturn', 'TR.PRICECLOSE'],

interval="1D",

start="2021-10-01",

end="2021-10-11")

DEX2Df

| VOD.L | BARC.L | TRI.N | ||||

| Total Return | Price Close | Total Return | Price Close | Total Return | Price Close | |

| Date | ||||||

| 01/10/2021 | -0.970874 | 112.2 | -0.907173 | 187.88 | -0.289645 | 110.16 |

| 04/10/2021 | 1.4082 | 113.78 | -0.319353 | 187.28 | -0.67175 | 109.42 |

| 05/10/2021 | 0.773422 | 114.66 | 3.908586 | 194.6 | 0.923049 | 110.43 |

| 06/10/2021 | -2.651317 | 111.62 | -1.387461 | 191.9 | 1.213438 | 111.77 |

| 07/10/2021 | 0.734635 | 112.44 | 0.958833 | 193.74 | 1.673079 | 113.64 |

| 08/10/2021 | -0.302383 | 112.1 | 0.732941 | 195.16 | 0.228793 | 113.9 |

| 11/10/2021 | -0.303301 | 111.76 | 1.291248 | 197.68 | 0.412643 | 114.37 |

VBA

Private Sub cmdClearAll_Click()

ActiveCell.Select

Range("G10").Value = ""

Range("G21:J100").Value = ""

If Not myRData1 Is Nothing Then Set myRData1 = Nothing

If Not myRData2 Is Nothing Then Set myRData2 = Nothing

If Not MyDex2Mgr Is Nothing Then Set MyDex2Mgr = Nothing

End Sub

Private Sub cmdGetRating_Click() On Error GoTo errHandler

ActiveCell.Select

[G7].Value = "" ' Note the use of CreateReutersObject - function in the PLVbaApis module. If MyDex2Mgr Is Nothing Then Set MyDex2Mgr = CreateReutersObject("Dex2.Dex2Mgr")

' Must call Initialise() at once m_cookie = MyDex2Mgr.Initialize() ' We can then create an RData object Set myRData1 = MyDex2Mgr.CreateRData(m_cookie)

With MyDex2Mgr .SetErrorHandling m_cookie, DE_EH_STRING ' Could also use DE_EH_ERRORCODES End With

' Set the properties & methods for the DEX2Lib.RData object With myRData1 .InstrumentIdList = [C6].Value ' Could use "TRI.N", "TRI.N; GOOG.O; MSFT.O" or array, e.g. arrInstrList. .FieldList = [C7].Value '"EJV.GR.Rating" ' Could use "RI.ID.RIC", "RI.ID.RIC; RI.ID.WERT" or array, e.g. arrFldList. .RequestParam = [C8].Value '"RTSRC:S&P" 'N.B. Could use .SetParameter "TRI.N; MSFT.O","RF.G.COMPNAME; RF.G.NUMEMPLOY; RF.G.CNTEMAIL", "", "RH:In CH:Fd Transpose:Y" 'Hence .SetParameter [InstrumentIDList].Value, [FieldList].Value, [RequestParam].Value, [DisplayParam].Value

'Ignore cache; get data directly from the Snapshot Server '.Subscribe False 'Or use cache by default .Subscribe End With Exit Sub

errHandler: MsgBox MyDex2Mgr.GetErrorString(Err.Number) End Sub

' OnUpdate event callback for myRData1 Private Sub myRData1_OnUpdate(ByVal DataStatus As Dex2Lib.DEX2_DataStatus, ByVal Error As Variant) Dim res As Variant

'Debug.Print DataStatus

If Error <> 0 Then [G10].Value = Error: Exit Sub

' get the data retrieved from the database res = myRData1.Data

' Display the result. [G10].Value = res End Sub

Private Sub cmdGetHistoryOfRating_Click() On Error GoTo errHandler

ActiveCell.Select

Range("G21:J100").ClearContents If MyDex2Mgr Is Nothing Then Set MyDex2Mgr = CreateReutersObject("Dex2.Dex2Mgr")

' Must call Initialise() at once m_cookie = MyDex2Mgr.Initialize() ' We can then create an RData object Set myRData2 = MyDex2Mgr.CreateRData(m_cookie)

With MyDex2Mgr .SetErrorHandling m_cookie, DE_EH_STRING ' Could also use DE_EH_ERRORCODES End With

' Set the properties & methods for the DEX2Lib.RData object With myRData2 .InstrumentIdList = [C15].Value .FieldList = [C16].Value .RequestParam = [C17].Value .DisplayParam = [C18].Value

'N.B. Could use .SetParameter "TRI.N; MSFT.O","RF.G.COMPNAME; RF.G.NUMEMPLOY; RF.G.CNTEMAIL", "", "RH:In CH:Fd Transpose:Y" 'Hence .SetParameter [InstrumentIDList].Value, [FieldList].Value, [RequestParam].Value, [DisplayParam].Value

'Ignore cache; get data directly from the Snapshot Server '.Subscribe False 'Or use cache by default .Subscribe End With Exit Sub

errHandler: MsgBox MyDex2Mgr.GetErrorString(Err.Number) End Sub

Python

Things are much simpler in Python:

rating = rd.get_history(

universe=['GB137283921='],

fields=['TR.IR.RatingSourceDescription', 'TR.IR.RatingSourceType',

'TR.IR.Rating'],

interval="1Y",

start="2015-01-25",

end="2023-02-01")

rating

GB137283921= |

Rating Source Description | Rating Source Type | Issuer Rating |

| Date | |||

| 17/12/2015 | Egan-Jones Commercial Paper | EJC | A1 |

| 17/12/2015 | Egan-Jones Senior Unsecured | EJU | BBB+ |

| 06/07/2016 | Egan-Jones Senior Unsecured | EJU | BBB |

| 04/10/2018 | Fitch Subordinated | FBD | BBB- |

| 26/11/2019 | Egan-Jones Senior Unsecured | EJU | BBB- |

| 29/07/2021 | Fitch Commercial Paper | FCP | F2 |

| 25/11/2022 | Egan-Jones Commercial Paper | EJC | A1 |

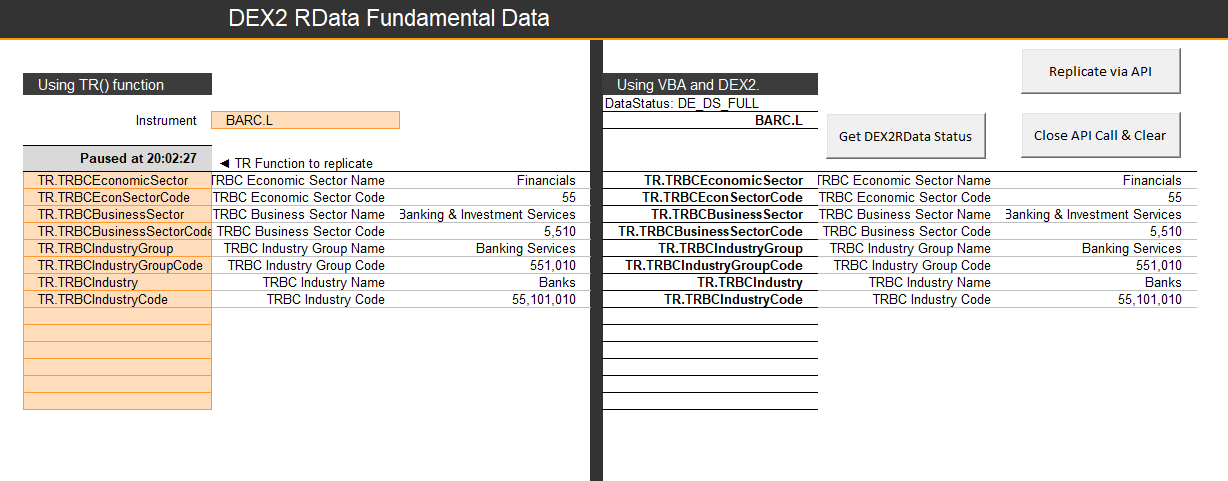

DEX2 Fundamental and Reference

Time Series data as the name suggests changes with time. Reference data, on the other hand, does not primarily change with time; when it does, it usually accounts for a structural change in the instrument at play (e.g.: a company changes from banking to tech operation industries or is acquired and changes name etc). Fundamental data is released temporally say quarterly or half-yearly or annually and is usually looked at across time eg Revenue or Sales. DEX2 provides access to all of our TR fields - which allow you to specify begin dates and end dates amongst other parameters. Access to these is unchanged in our new APIs - only its a lot simpler.

VBA

In VBA, after creating 'Private MyDex2Mgr As Dex2Lib.Dex2Mgr':

Private MyDex2Mgr As Dex2Lib.Dex2Mgr

Private MyDex2MgrADC As Dex2Lib.IDex2Mgr2

Private MyDex2Cookie As Long

' Private variable that holds the Dex2 RData, able to obtain TR fields.

Private WithEvents MyDex2RData As Dex2Lib.RData

to complete the Tutorial 6 example, one could go through the following to collect DEX2 Fundamental and Reference data:

' Now create the Dex2 and IDex2 objects.

Set MyDex2Mgr = CreateDex2Mgr()

Set MyDex2MgrADC = MyDex2Mgr

' Initialise using the DE_MC_ADC_POWERLINK enumeration

MyDex2Cookie = MyDex2MgrADC.Initialize(DE_MC_ADC_POWERLINK)

' And create an RData object.

Set MyDex2RData = MyDex2Mgr.CreateRData(MyDex2Cookie)

With MyDex2RData

.InstrumentIDList = Range("G6").Value ' Or for multiple isntruments "TRI.N;MSFT.O;GOOG.O"

.FieldList = strInstrList ' Or single field "TR.CLOSE"

.RequestParam = "" ' Or of the form "edate:-20d sdate:-9d"

.DisplayParam = "CH:Fd" ' Or of the form "RH:In CH:Fd"

'' OR can use .SetParameter

'.SetParameter Range("G6").Value, strInstrList, "", "CH:Fd"

' Send the query without using cache

.Subscribe False ' Or use cache by default - myDex2RData.Subscribe

' When the data is returned, the myDex2RData_OnUpdate event and Sub are 'fired'.

Python

Fundamental data was covered above under 'RData Fundamentals'; such data can be found in Python with RD (and rd.get_data, rd.get_history or rd.content.fundamental_and_reference.Definition) or EDAPI.

Fundamental and Reference Timeseries

VBA

DEX2 Fundamental and Reference Timeseries data could be fetched similarly to simple time series data:

Start with

' Private Variable that holds the instance of the Dex2 manager singleton

Private MyDex2Mgr As Dex2Lib.Dex2Mgr

Private MyDex2MgrADC As Dex2Lib.IDex2Mgr2

' Private variable that holds the cookie that identifies the Dex2 session Private MyDex2Cookie As Long ' Private variable that holds the Dex2 RData Private WithEvents MyDex2RData As Dex2Lib.RData ' Private variable that holds the Dex2 RDataMgr Private MyDex2RDataMgr As Dex2Lib.RDataMgr

' Private variable that holds the Dex2 logger Private MyDex2Logger As CLogger

Then initialise clicks:

' Instantiate the Dex2 manager

Set MyDex2Mgr = CreateDex2Mgr()

Set MyDex2MgrADC = MyDex2Mgr

' Instantiate the RSearch logger

Set MyDex2Logger = New CLogger

' Initialize Dex2 session

MyDex2Cookie = MyDex2MgrADC.Initialize(DE_MC_ADC_POWERLINK, MyDex2Logger)

' We can choose to display error code

MyDex2Mgr.SetErrorHandling MyDex2Cookie, DE_EH_ERROR_CODES

' Or display error description

' MyDex2Mgr.SetErrorHandling MyDex2Cookie, DE_EH_STRING

' Create a Dex2 query using the session cookie

Set MyDex2RData = MyDex2Mgr.CreateRData(MyDex2Cookie)

' Create a Dex2 query manager using the session cookie

Set MyDex2RDataMgr = MyDex2Mgr.CreateRDataMgr(MyDex2Cookie)

Then, after some error & event handling:

' Set input values

MyDex2RData.SetParameter _

Range("Dex2Item").Value, _

Range("Dex2Fields").Value, _

Range("Dex2RequestParameters").Value, _

Range("Dex2DisplayParameters").Value

' Or using the following individual properties

' MyDex2RData.InstrumentIDList = Range("Dex2Item").Value

' MyDex2RData.FieldList = Range("Dex2Fields").Value

' MyDex2RData.requestParam = Range("Dex2RequestParameters").Value

' MyDex2RData.displayParam = Range("Dex2DisplayParameters").Value

' Send the query without using cache MyDex2RData.Subscribe (False) ' Or use cache by default ' MyDex2RData.Subscribe

Before creating 'OnUpdate' code.

This is all quite heavy in VBA, while it could hardly be simpler in Python:

Python

This was covered above, in the section 'RData Fundamentals' using RD's rd.get_history function. We can also do this with the rd.get_data function:

DEX2TrDf = rd.get_data(

['VOD.L', 'MSFT.N', 'TRI.N'],

fields=[

'TR.RevenueMean.date', 'TR.RevenueMean', 'TR.TRBCEconomicSector', 'TR.TRBCEconSectorCode',

'TR.TRBCBusinessSector', 'TR.TRBCBusinessSectorCode', 'TR.TRBCIndustryGroup',

'TR.TRBCIndustryGroupCode', 'TR.TRBCIndustry', 'TR.TRBCIndustryCode'],

parameters={'SDate': 0, 'EDate': -3, 'FRQ': 'FY'})

DEX2TrDf

| Instrument | Date | Revenue - Mean | TRBC Economic Sector Name | TRBC Economic Sector Code | TRBC Business Sector Name | TRBC Business Sector Code | TRBC Industry Group Name | TRBC Industry Group Code | TRBC Industry Name | TRBC Industry Code | |

| 0 | VOD.L | 14/02/2023 | 45864975420 | Technology | 57 | Telecommunications Services | 5740 | Telecommunications Services | 574010 | Wireless Telecommunications Services | 57401020 |

| … | … | … | … | … | … | … | … | … | … | … | … |

| 8 | TRI.N | 22/02/2023 | 6937020650 | Industrials | 52 | Industrial & Commercial Services | 5220 | Professional & Commercial Services | 522030 | Professional Information Services | 52203070 |

| 9 | TRI.N | 01/02/2023 | 6626869820 | ||||||||

| 10 | TRI.N | 07/02/2022 | 6311529500 | ||||||||

| 11 | TRI.N | 22/02/2021 | 5980789530 |

Conclusion

In conclusion, we can see that the Office COM API had many great uses, but limitations too. This was without mentioning its reliability on DLLs that can be heavy to run on a personal machine. But the Refinitiv Python Libraries (RD, RDP and EDAPI) can not only replicate these COM functionalities but enhance them in many instances, the simplest example being the Historical News functionality shown above.

Several COM API functionalities relying on a technology called Adfin was not replicated in Python in this article, but we will investigate them in another article - so stay tuned!

Further Resources

COM APIs: Overview | Quickstart Guide | Documentation | Downloads | Tutorials | Q&A Forum

RD Library: Overview | Quickstart Guide | Documentation | Tutorials | Q&A Forum